May saw significant bullish momentum in crypto markets as Bitcoin (BTC) reached a new all-time high above $111,000 and Coinbase joined the S&P 500.

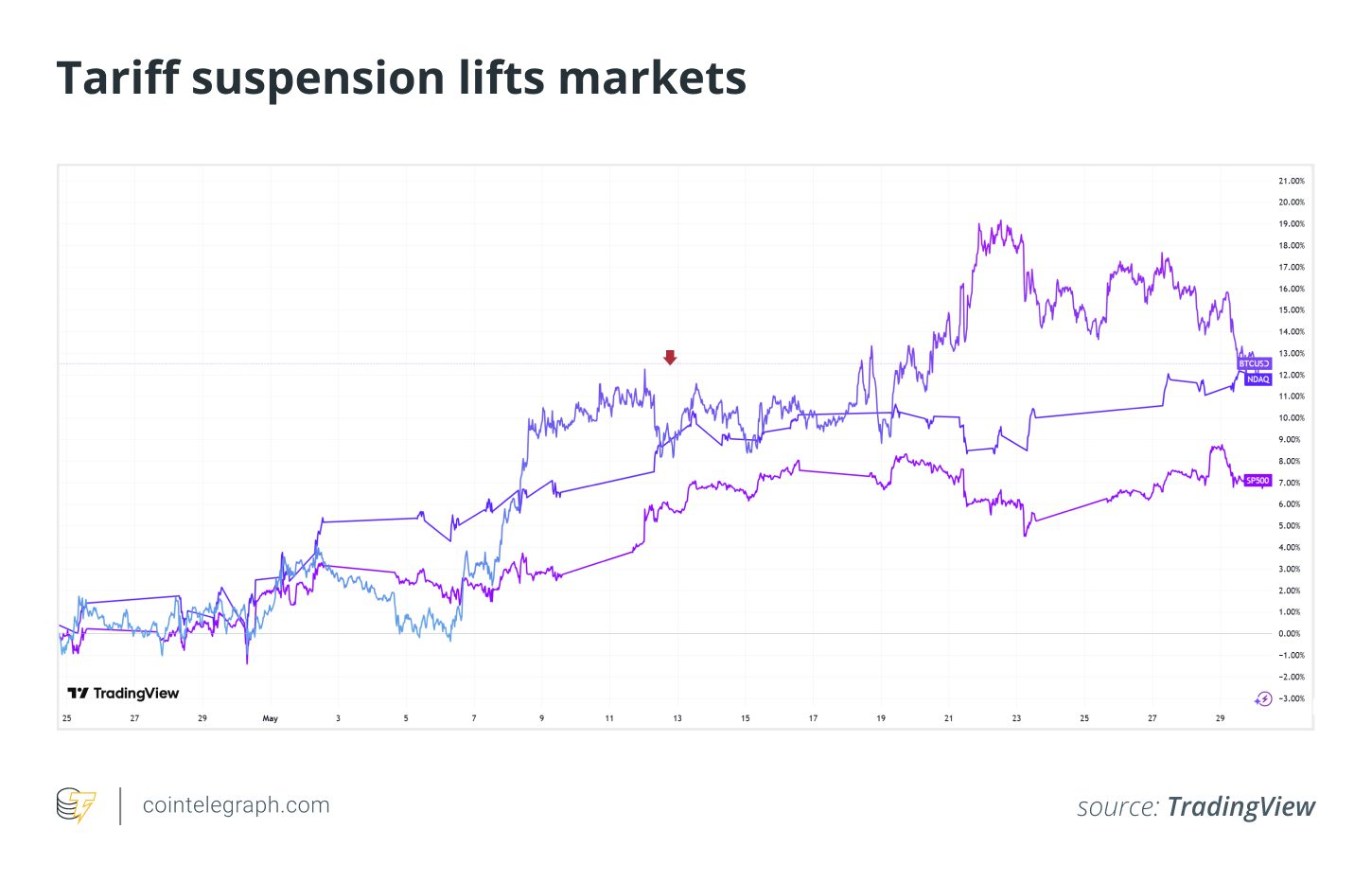

Markets experienced some relief when, on May 12, news of a US-China trade deal surfaced, temporarily pausing tariff increases that had previously unsettled the markets. This news briefly pushed BTC price to $105,000, a three-month high, before retracing to around $102,000.

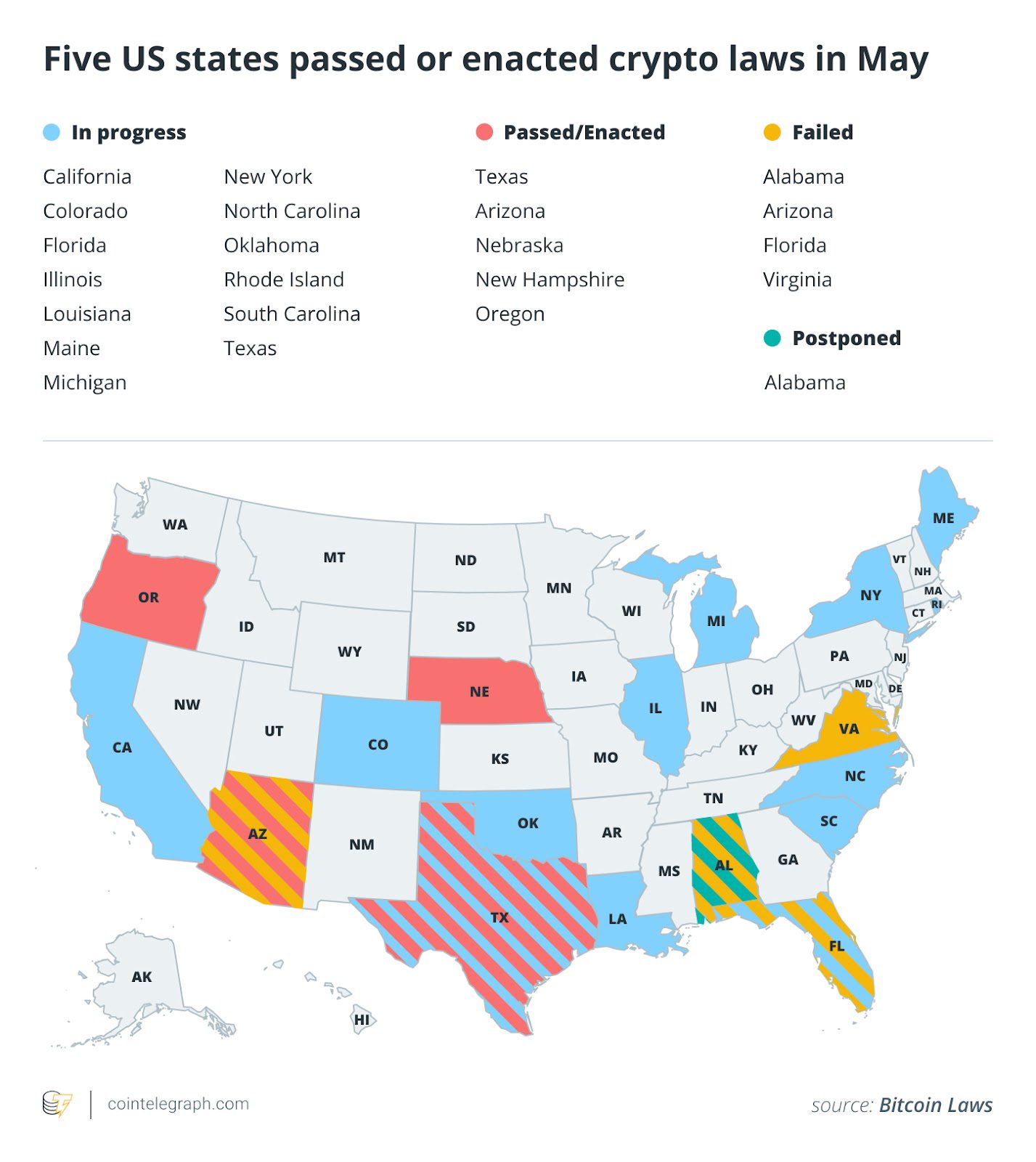

On the regulatory front, five US states enacted new Bitcoin laws. Texas established a long-awaited state Bitcoin reserve. In Alabama, an effort to exempt crypto from certain forms of taxation was indefinitely postponed.

OpenAI is also planning expansion into the US, setting up eye-scanning Orb stations across six cities in five American states. This move follows legal challenges against Worldcoin in multiple countries.

Here’s May by the numbers:

Five states enact crypto-related laws in May, Texas passes Bitcoin reserve bill

In the US, cryptocurrency legislation is progressing across various states, with five states passing or enacting cryptocurrency-related bills.

In Texas, a bill was passed to establish a state Bitcoin (BTC) reserve. New Hampshire took a similar step, enabling the state treasurer to invest public funds in precious metals and digital assets like Bitcoin through the passage of HB302.

In Arizona, the newly created Bitcoin and Digital Assets Reserve Fund will hold unclaimed digital assets. The state can now claim ownership of abandoned digital assets if the owner doesn’t respond to contact attempts for three years. Arizona can also stake these assets to earn airdrops and rewards.

In Nebraska, public power utilities now have some control over Bitcoin miners. LB526, passed on May 14, allows them to require Bitcoin miners using 1 megawatt or more of power to cover the cost of infrastructure upgrades. It also introduces a permit regime and reporting requirements for power consumption.

Oregon has included crypto in its Uniform Commercial Code.

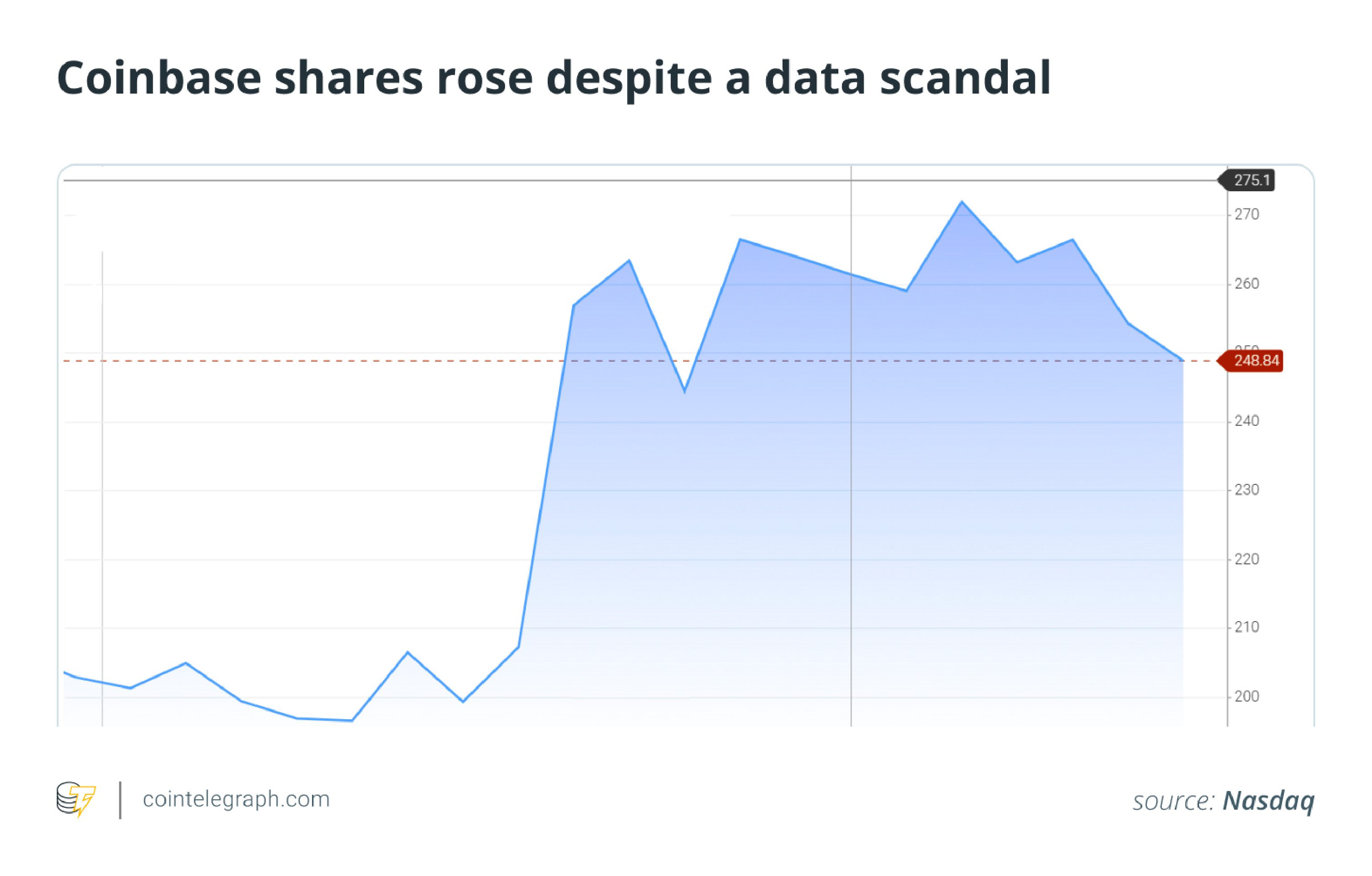

Coinbase stock up 19.37% in May, joins S&P 500

The stock price of crypto exchange Coinbase increased by 19.37% over the month, despite disclosing a $400 million security incident on May 15.

Despite the significant sum involved in the attack, which reportedly triggered an investigation by the US Department of Justice, the stock price closed May 29 at $248.84.

Furthermore, Coinbase became the first crypto company to be included in the S&P 500 Index, hailed by the crypto industry as a major milestone for crypto adoption and growth.

However, not everyone is enthusiastic. Concerns about security and market volatility have led some observers to question the exchange’s inclusion in the index. Business and economics commentator Ed Elson stated, “All I can tell you is this is not good.”

Major indexes bounce back after 90-day US-China tariff deal

On May 12, the US administration announced a 90-day suspension of tariffs in a deal with China, resulting in the S&P 500 and the Nasdaq seeing gains of 4.5% and 3%, respectively, the following day. Bitcoin also rose by 2%.

According to market analysis, Bitcoin did not perform as well as expected in the days following the announcement, as macroeconomic conditions favored stocks over Bitcoin or gold. Gold fell by 3.4% on May 12.

Before trading opened on May 30, the Nasdaq-100 index was up 9.16% for the month, while the S&P 500 climbed 6.16%.

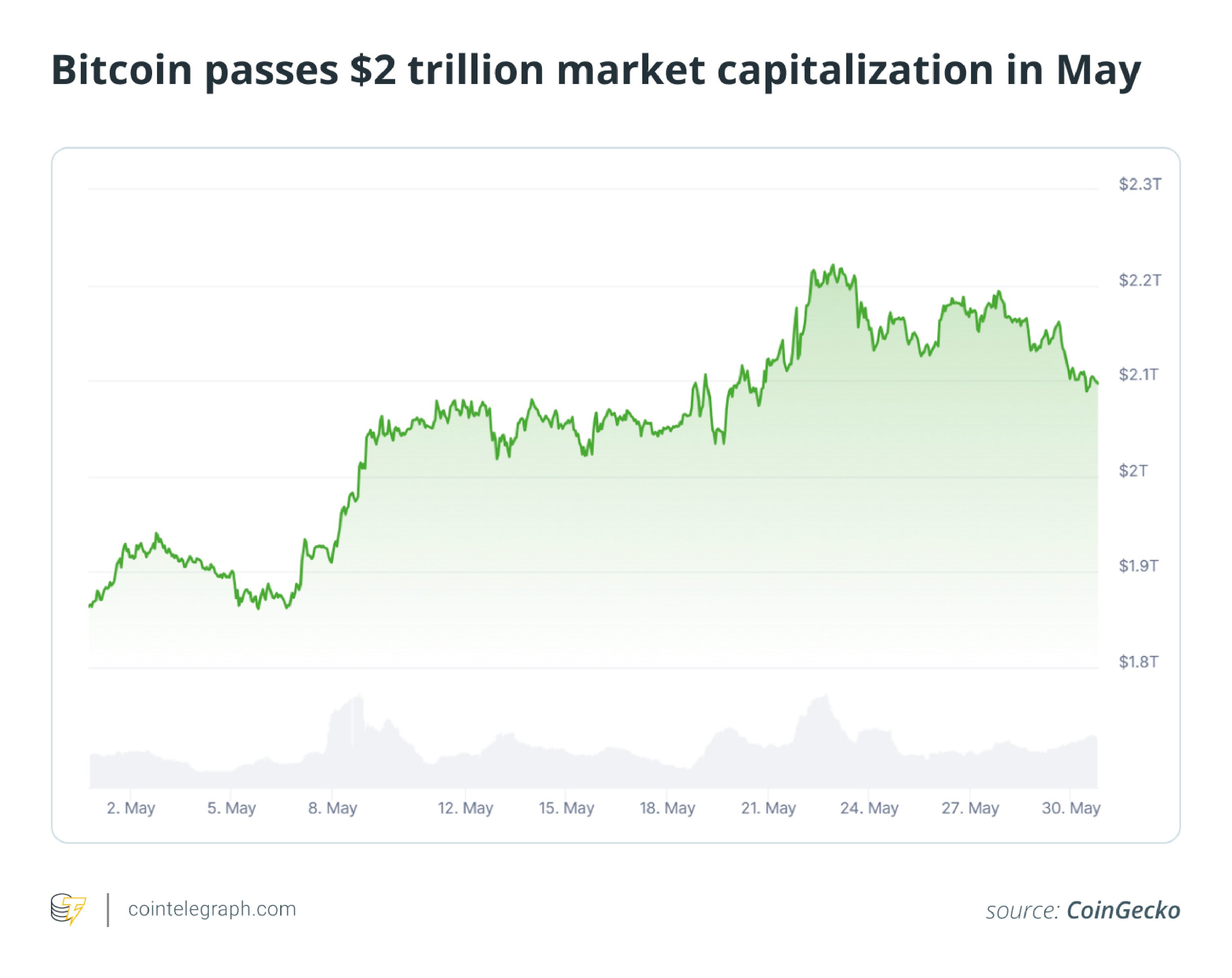

Bitcoin “Pizza Day” sees market cap top Amazon at $2.2 trillion, BTC ATH

On May 22, “Bitcoin Pizza Day,” Bitcoin’s market capitalization surpassed $2.2 trillion, exceeding the market cap of Amazon.

Bitcoin Pizza Day, commemorating Laszlo Hanyecz’s 10,000 BTC pizza purchase in 2010 (worth $41 at the time), also saw Bitcoin hit a new all-time high at just over $109,000. Bitcoin then broke that record a few days later, reaching $111,970.

By the end of May, Bitcoin’s rally had cooled, with spot Bitcoin ETFs recording $347 million in net outflows on May 29, ending a 10-day inflow streak.

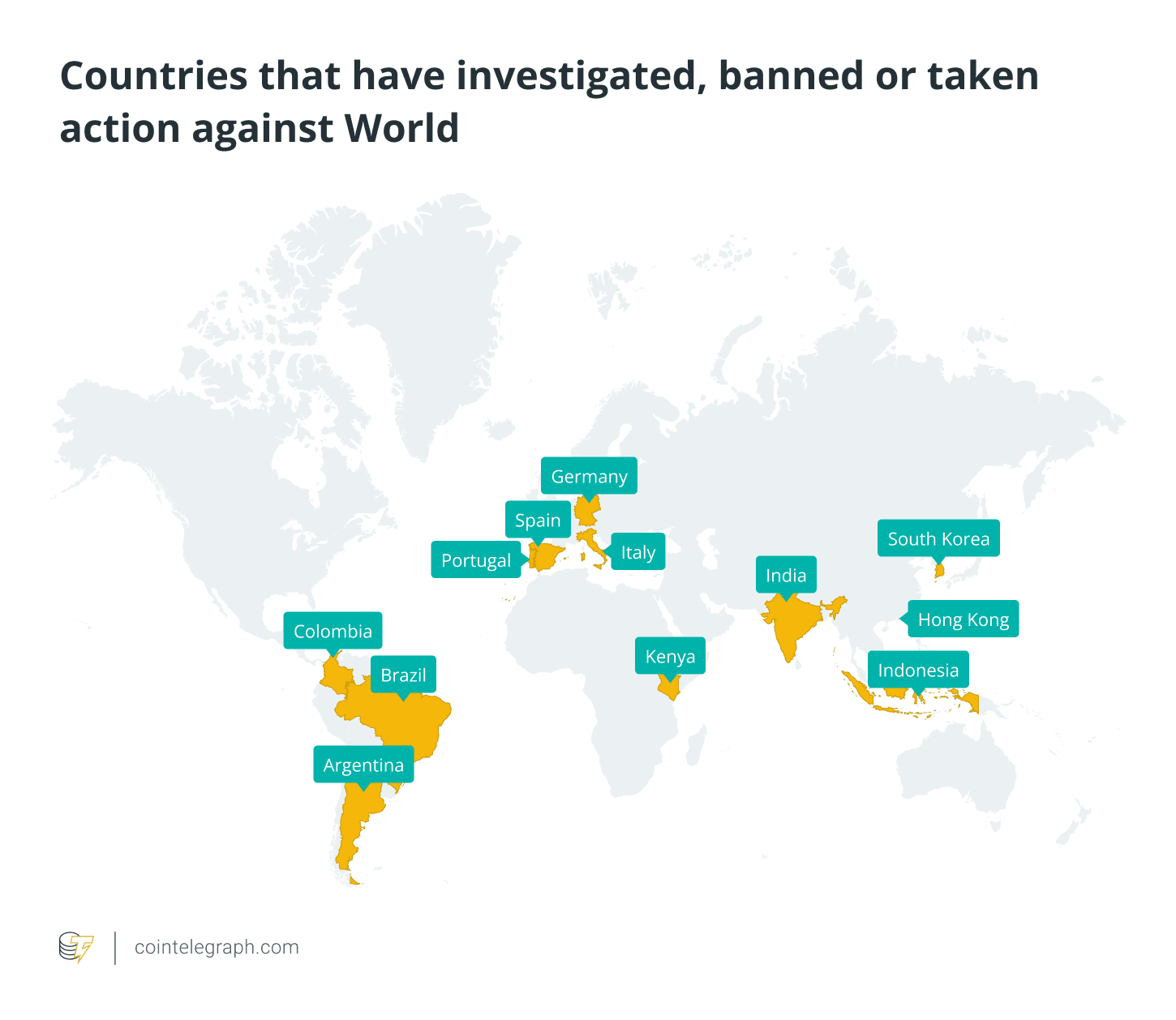

OpenAI moves world project to US after enforcement actions in 12 countries

On April 30, OpenAI CEO Sam Altman announced that his company’s digital identity project, Worldcoin, would be setting up in the United States.

Regulators in 12 countries have taken legal action against Worldcoin, citing concerns ranging from data privacy (Kenya) to potential economic manipulation (Brazil). Hong Kong has banned the project outright.

Worldcoin has addressed privacy concerns by stating that it holds no identifying information linked to the eye scan data recorded by its Orb devices. They maintain that users own and control their information in the form of their World ID.